Introduction to Reinsurance

Reinsurance is insurance for insurance companies. Insurers (cedants) transfer part of their risk to reinsurers in exchange for a reinsurance premium, reducing exposure to large or unexpected losses. It strengthens insurers’ financial stability, provides capital relief, and enables them to underwrite larger and more complex risks at sustainable costs.

The two main forms of reinsurance are:

• Treaty Reinsurance – Portfolio-based protection.

• Facultative Reinsurance – Risk-specific placement.

Market conditions are typically described as a hard market (rising prices due to heavy losses or reduced capital) or a soft market (abundant capacity leading to increased competition and more favourable pricing).

2026 Thailand Renewal Overview

The 2026 renewal season for Thailand was marked by significant challenges and structural repricing, particularly across Property and Motor Excess of Loss (XOL) programs. The primary drivers were two major natural catastrophe events occurring within a single year.

Seismic Loss Event – Myanmar Earthquake Impacting Bangkok

On 28 March 2025, a powerful earthquake originating more than 1,000 km away in Myanmar sent vibration as far as Bangkok. Due to the city’s soft soil conditions, high-rise structures—particularly condominiums as well as some commercial buildings and hotels—were severely affected. Although only one building collapsed, widespread non-structural damage (i.e cracks, burst pipes, elevator, etc) resulted in total market estimated insured losses exceeding THB 60 billion. This event prompted insurers, catastrophe modelers, and reinsurers to reassess their risk models, with Bangkok’s soft soil identified as a key amplifying factor in both vibration intensity and duration.

Devastating Floods in Southern Thailand

Midway through the treaty reinsurance renewal season, extreme flooding struck southern Thailand during Nov–Dec 2025. The rainfall intensity was extraordinary—approximately 600 mm over just three days, equating to an estimated 300-year return period. Hat Yai, one of the largest regional commercial hubs in southern Thailand, was almost entirely inundated, with flood depths reaching 2–4 metres. Losses extended well beyond buildings and contents, with thousands of vehicles submerged and largely declared total losses. This event is also forcing the industry to recalibrate flood assumptions and models, as severe flash floods appear to be occurring more frequently than previously anticipated.

Market Impact and Outlook

Supported by the resilience of the reinsurance system, these shock losses are being absorbed without systemic disruption. However, Thailand’s property and motor XOL programs covering Natural Perils are now clearly in a deficit position, with participated reinsurers facing payback periods estimated at 10 to 30 years. As a result, meaningful premium increases are inevitable and are expected to pass to the primary market.

Fortunately, the broader global reinsurance environment at the 2026 renewal remains relatively supportive. Global softening market sentiment continues to be influenced by excess capacity, historically low global reinsured catastrophe losses over the past decade, and strong reinsurer profitability. Adequate capacity remains available and is expected to be deployed selectively at technically adequate pricing levels.

In contrast, the proportional treaties renewals in Thailand were competitive at 1 Jan 26 to be favourable to Thai cedants as almost proportional treaties are excluded natural catastrophe.

Conclusion

The 2026 renewal demonstrates a clear divergence between Non-Proportional (XOL) and Proportional markets. While XOL pricing has hardened significantly due to major catastrophe losses, proportional treaties remain competitive with ample capacity. Thai cedants face higher catastrophe protection costs but continue to benefit from strong global reinsurance system resilience.

Key Renewal Findings

Non-Proportional Treaty (XOL) Property – Impact of EQ and Flood

- Most Property excess of loss (XOL) programs in Thailand continue to be purchased on a combined risk and catastrophe basis, providing cover for gross losses from natural perils, as proportional treaties generally exclude natural perils.

- The 1 Jan 2026 property and motor XOL renewal season was challenging and protracted. As expected, sharp increasing XOL price were most pronounced for property XOL and, following by motor XOL after flood losses in southern Thailand during Nov – Dec 2025.

- The renewal process was dragged into late December, with several reinsurers revising or withdrawing earlier quotations issued prior to the southern flood event. This resulted in delays to firm order terms (FOTs) and slower authorization of capacity as reinsurers waited for updated submissions of estimated losses from the southern flood.

- Within the Property XOL market, underwriting approaches diverged notably between incumbent reinsurers that had incurred losses in 2025 and new or returning markets seeking to grow premium volumes. Incumbent markets generally pursued substantial rate increases to reflect loss experience and anticipated payback requirements. In contrast, new capacity viewed prevailing conditions as offering attractive pricing opportunities and was prepared to support programmes based on independent assessments of pricing adequacy. As a result, quoting behaviour from new markets was generally more measured and commercially competitive compared with incumbents.

- Initial quotations—predominantly from incumbent reinsurers—were materially above cedants’ expectations, in some cases up to double the expiring levels. This prompted increased engagement with alternative markets and, in certain instances, the appointment of additional brokers to secure more competitive outcomes.

- Despite extensive negotiations and late placements, the majority of XOL programs were completed on time with some programs on the last day before inception with full market capacity supported by both expiring and new markets.

Key Renewal Findings

Non-Proportional Treaty (XOL) Property – Impact of EQ and Flood

- Most Property excess of loss (XOL) programs in Thailand continue to be purchased on a combined risk and catastrophe basis, providing cover for gross losses from natural perils, as proportional treaties generally exclude natural perils.

- The 1 Jan 2026 property and motor XOL renewal season was challenging and protracted. As expected, sharp increasing XOL price were most pronounced for property XOL and, following by motor XOL after flood losses in southern Thailand during Nov – Dec 2025.

- The renewal process was dragged into late December, with several reinsurers revising or withdrawing earlier quotations issued prior to the southern flood event. This resulted in delays to firm order terms (FOTs) and slower authorization of capacity as reinsurers waited for updated submissions of estimated losses from the southern flood.

- Within the Property XOL market, underwriting approaches diverged notably between incumbent reinsurers that had incurred losses in 2025 and new or returning markets seeking to grow premium volumes. Incumbent markets generally pursued substantial rate increases to reflect loss experience and anticipated payback requirements. In contrast, new capacity viewed prevailing conditions as offering attractive pricing opportunities and was prepared to support programmes based on independent assessments of pricing adequacy. As a result, quoting behaviour from new markets was generally more measured and commercially competitive compared with incumbents.

- Initial quotations—predominantly from incumbent reinsurers—were materially above cedants’ expectations, in some cases up to double the expiring levels. This prompted increased engagement with alternative markets and, in certain instances, the appointment of additional brokers to secure more competitive outcomes.

- Despite extensive negotiations and late placements, the majority of XOL programs were completed on time with some programs on the last day before inception with full market capacity supported by both expiring and new markets.

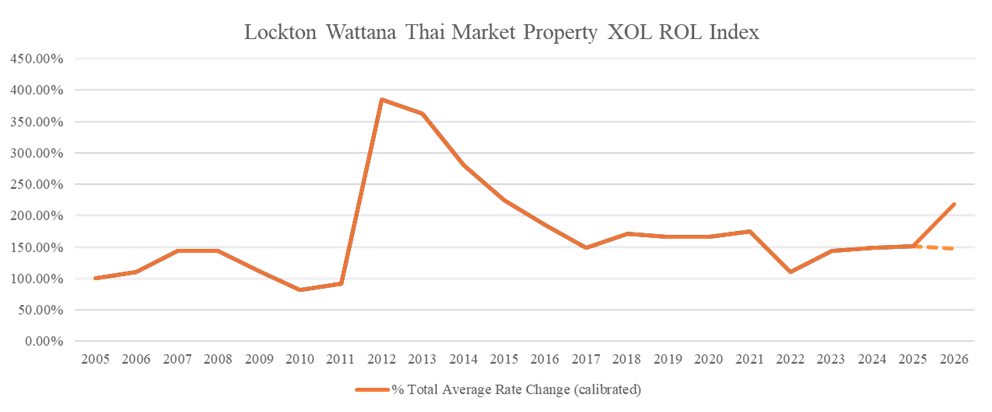

The average ROL across all Property XOL programmes was calculated on an inclusive basis, including Whole Account XOL. This was then calibrated to the expiring limit to ensure like-for-like comparison, recognising that ROLs on newly added top layers are materially lower than those on underlying layers.

As at 1 January 2026, the Thai market Property XOL averaged pricing index increased by approximately 45%.

Loss-affected XOL programmes experienced risk-adjusted rate increases ranging from 30% to 100%. With the exception of a small number of loss-free programmes, risk-adjusted rates generally increased by around 5%.

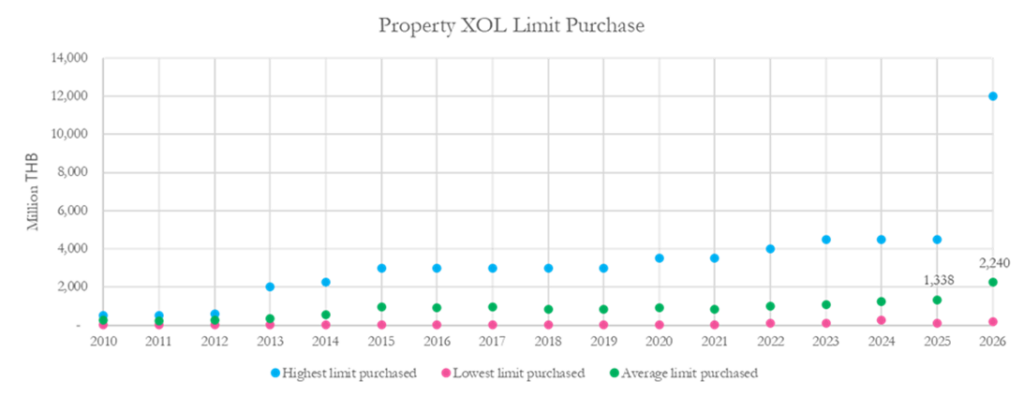

- Most Thai insurers opted for higher levels of protection, purchasing limits up to a 250-year return period. There are currently no minimum regulatory requirements for catastrophe reinsurance coverage in Thailand; however, insurers typically purchase natural catastrophe protection equivalent to a 1-in-200 to 1-in-250-year return period, subject to individual risk appetite and budget constraints.

- At the 1 January 2026 renewal, the average purchasing limit has increased from 1.338 billion baht (2025) to 2.240 billion baht (2026)

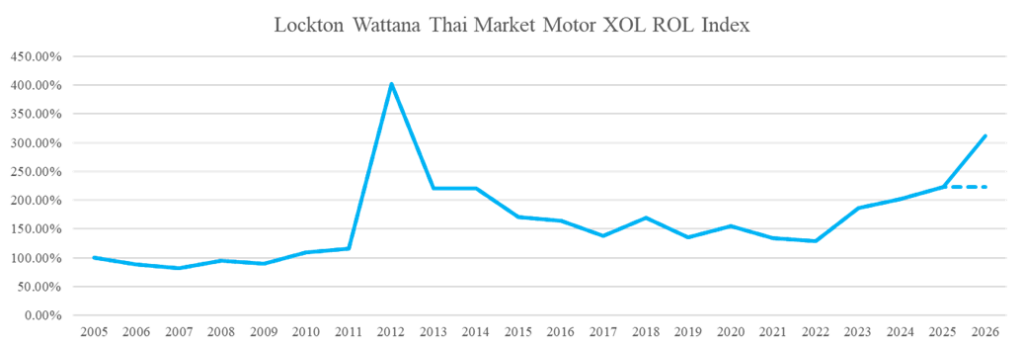

- As at 1 January 2026, the Thai Motor XOL pricing index increased by approximately 40% year-on-year on average.

- In contrast to the property market, Motor XOL capacity tightened rapidly as Thai insurers increased their purchased limits. With fewer new reinsurers entering the market compared to the Property XOL segment, competitive quotations from new markets were limited, and pricing dynamics were largely driven by incumbent reinsurers.

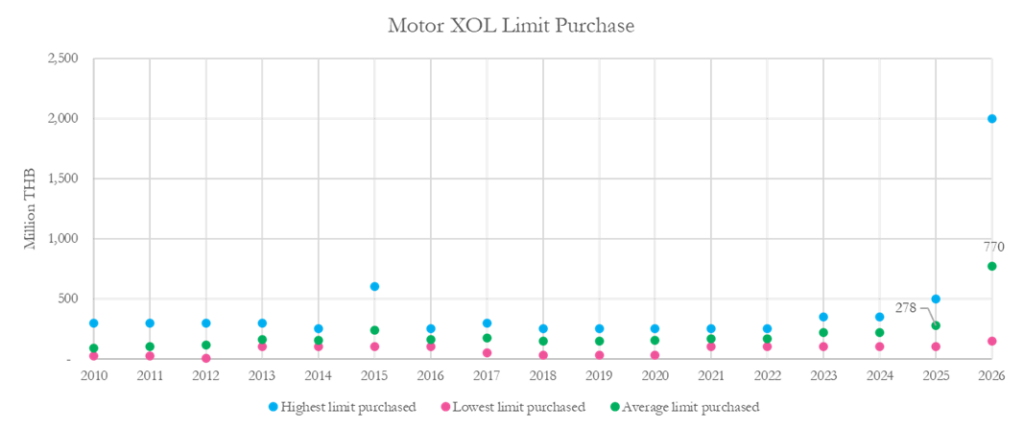

- Similar to property XOL program, most Thai insurers opted for higher levels of protection, purchasing limits.

- At the 1 January 2026 renewal, the average purchasing limit has increased from 278 million baht (2025) to 770 million baht (2026)

Key Renewal Findings

Proportional Bouquet Treaty

In contrast to the hardening sentiment in the XOL market, proportional treaty business clearly transitioned into a softening phase at this renewal, particularly for programmes with strong historical performance. The degree of softening varied by account, with outcomes largely influenced by individual loss experience.

The majority of proportional programmes continued to deliver positive results, enabling cedants to negotiate marginally improved renewal terms, including higher commissions and increased capacity. Improvements in ceded commissions reflected both higher ceding commissions and a narrowing of previously imposed loss participation clauses (LPCs). Programmes that had been subject to less favourable ceding commissions and LPCs in prior years generally saw greater scope for improvement.

Capacity for proportional business was ample despite some margin compression for reinsurers. Available capacity improved materially as reinsurers demonstrated increased appetite, particularly where property programmes were written on a risk-only basis and excluded natural perils. Oversubscription was common, exceeding 150% and reaching up to 200% on certain programmes at the 1 January 2026 renewal.

Reinsurers were generally more solution-oriented in addressing cedants’ requests, in contrast to the more defensive approach seen during the hardening phase in previous years. Many reinsurers sought to increase their participations through higher authorised lines, with existing markets expanding expiring shares and new reinsurers entering the proportional segment.

No new restrictive terms and conditions were introduced for 2026, and there was some flexibility for clients to reinstate coverage that had been reduced or removed during the market hardening of recent years.